We’ve all felt it — rising food costs, stubbornly high housing prices, and unpredictable energy bills. Even as we move deeper into 2025, inflation continues to shape the US economy and the financial decisions we make every day.

But what’s really driving inflation today? And why, after years of aggressive policy moves, hasn’t it fully cooled? Let’s break it down — looking at what’s happening now, the lessons we can draw from the past, and how we can position ourselves as investors.

Inflation-Ready Checklist

Learn what to do with your money during inflationary times

What is Inflation?

Inflation refers to the devaluing of a currency’s buying power which leads to an intentional increase in the price of goods and services.

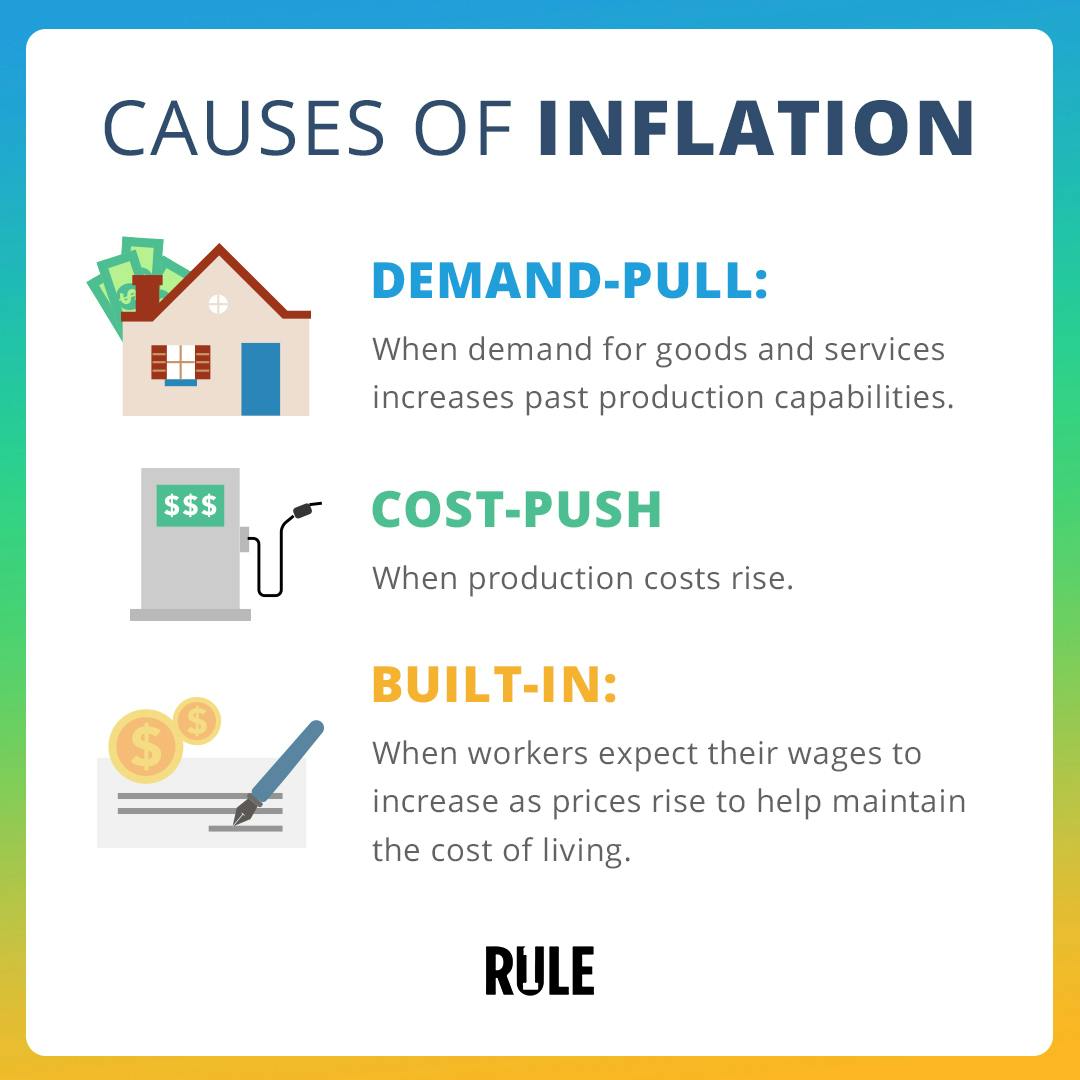

There are three different types of inflation that can be triggered in different ways.

Demand-pull inflation: This happens when the demand for goods and services exceeds what the economy can produce. It’s like when consumers flood into the market with stimulus checks (as we saw in 2020–2021), causing shortages and pushing prices up.

Cost-push inflation: This occurs when the cost of raw materials or wages rises, forcing companies to pass those costs on to consumers. We’ve seen this most dramatically in oil, gas, and food prices.

Built-in inflation: This is when workers and businesses expect prices to keep rising, so wages and prices go up in a self-reinforcing loop.

What Causes Inflation?

Inflation always comes down to two things: an increase in the money supply and a decrease in the currency’s purchasing power.

Looking back, during the COVID-19 pandemic, the US government printed trillions in stimulus aid to keep the economy afloat. While this supported households and businesses, it also injected massive liquidity into the system, contributing to rapid inflation.

Current Inflation Trends

As we stand in 2025, inflation has come down from the alarming 9% peaks we saw in 2022 but still hovers stubbornly around 2.8%, above the Federal Reserve’s 2% target.

The drivers today are different from just a few years ago:

Housing costs: Mortgage rates, while down slightly from their highs, remain elevated, and housing inventory is still tight. This has kept rents and home prices high.

Services inflation: Everything from healthcare to insurance to childcare continues to climb in price.

Energy volatility: Geopolitical tensions have rattled global oil and gas markets, making energy prices unpredictable.

Inflation-Ready Checklist

Learn what to do with your money during inflationary times

Major Events That Shaped Today’s Inflation

Reflecting on recent history helps explain where we are now.

The COVID-19 pandemic (2020–2021) disrupted global supply chains, reduced production, and led to unprecedented stimulus spending — all of which lit the initial inflationary fire.

The Federal Reserve’s response (2022–2024) involved a historic series of interest rate hikes, pushing borrowing costs to levels not seen in decades. While this cooled demand, it didn’t fully tame inflation.

The Inflation Reduction Act (2022) was the largest government investment in climate and energy in US history. While it aimed to lower costs over time through clean energy incentives, its economic impact is still unfolding — and its near-term effect on inflation has been modest at best.

Labor Market and Wage Dynamics

Today’s labor market remains surprisingly resilient. Unemployment remains low, though wage growth has cooled from the hot pace of 2022–2023. While that’s helped moderate some price pressures, strong consumer demand has kept upward pressure on essentials like housing, food, and services.

For retirees and those near retirement, this inflationary environment poses serious challenges. At just 3% annual inflation, the cost of living nearly doubles over 25 years. If, as some predict, inflation averages closer to 4–5%, the retirement savings needed to maintain your lifestyle could balloon to five or six million dollars for many households — up from the two million often cited a few years ago.

Housing: A Stubborn Source of Inflation

Housing remains one of the most persistent drivers of inflation. While home price growth has slowed, affordability remains a crisis. Mortgage rates, even after moderating, are still well above their pre-2022 levels, pricing out many first-time buyers. Tight inventory continues to fuel bidding wars on entry-level homes.

Historical Parallels

History gives us important context.

World War II and the Korean War saw demand-pull inflation as economies boomed and supplies ran short.

The 1970s were marked by cost-push inflation, where oil shocks and wage-price spirals drove prices higher.

The Iraq and Gulf Wars also saw oil price spikes, hitting consumers and businesses hard.

The 2008 housing crash reminds us how financial excess and loose lending can collapse markets — a cautionary tale that still influences housing policy today.

What’s different now is the combination of these pressures: persistent supply chain frictions, geopolitical tensions, and the legacy of pandemic-era stimulus.

Inflation Expectations and the Inflation Reduction Act

The Federal Reserve continues to project that inflation will remain elevated above its 2% target for years to come, even as aggressive interest rate hikes have helped cool some price pressures. While the Inflation Reduction Act, passed in 2022, laid the groundwork for long-term clean energy investments, its immediate effect on consumer prices has been modest.

Importantly, investor Ray Dalio has shifted his recent warnings away from specific inflation rate forecasts and toward the broader structural risks facing the U.S. economy. Dalio has expressed deep concern about the nation’s mounting debt burden, warning that without meaningful policy reforms, the U.S. could face a debt crisis that leads to higher interest rates, economic instability, and potentially renewed inflationary pressures.

For investors, this underscores the critical need to build resilient, inflation-aware portfolios. It’s no longer just about watching inflation numbers — it’s about understanding the deeper economic risks that can ripple through markets and affect retirement planning, wealth-building, and investment strategy.

How to Invest During Inflation

Inflation isn’t just a problem — it’s an environment you can navigate. And here’s where the Rule #1 philosophy comes in.

Our message is clear: diversification alone won’t protect you. Instead, focus on:

Wonderful businesses: Companies with durable competitive advantages (moats), pricing power, and strong cash flow.

Commodities and sectors that benefit from inflation: Think energy, agriculture, and select industrials.

Your own education: Learn how to assess companies, read financial statements, and understand valuations.

And don’t forget to grab the Inflation-Ready Checklist to ensure your portfolio is built to last.

Final Takeaway

While inflation has moderated from its peak, it’s not going away anytime soon. The key for investors is to adapt: focus on businesses that can thrive in this environment, stay informed, and build a portfolio designed to preserve — and grow — your wealth over the long term.

Attend a Rule #1 Workshop

Learn how to conduct research, choose the right companies for you, and determine the best time to buy.

**Editor’s Note (Updated May 2025): This article was originally published in 2022 and has been significantly updated in 2025 to reflect current examples and Rule #1 investing insights.